It all started quite innocently, as most neighborhood problems do. We bought a house in Ourense, with a small plot where the remains of an old construction stand: just two stone walls, with no roof, no use, nothing.

One day, the neighbor Margarita told us that she had dampness in her house for many years and that, according to her, it came from our land. We tolde her we needed an expert report. That is the minimum needed to understand what is happening, assess whether there is any responsibility, and, if so, submit a claim to the previous owners, who had already told us that they would cooperate if a hidden defect could be proven.

She never gave us that report.

What did start appearing were different versions every time we spoke with her: that she had a report; that City Hall had ruled in her favor; that she had already reported the previous owners, none of it was true. Each visit turned into a new story and, little by little, into constant harassment.

City Hall eventually intervened. They conducted an official inspection in June 2025 and issued a report as clear as day:

- There was no visible dampness coming from our property.

- There was no structural risk.

- The property could not legally be declared a ruin.

City Hall saw it for what it was: an old construction in apparent good condition, which does not cause the problems she claimed.

Up to that point, one could think the matter was over, but this is where the nightmare begins.

As the situation with the neighbor was becoming unsustainable, we sent her a burofax informing that, from that moment on, everything should be handled through our lawyer. End of direct contact.

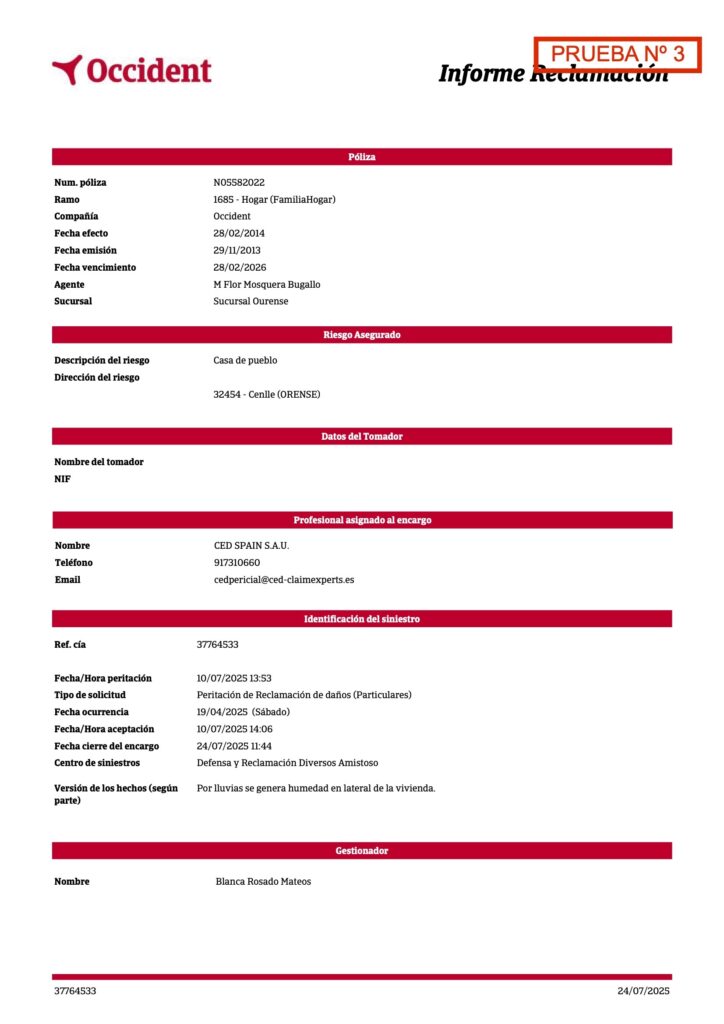

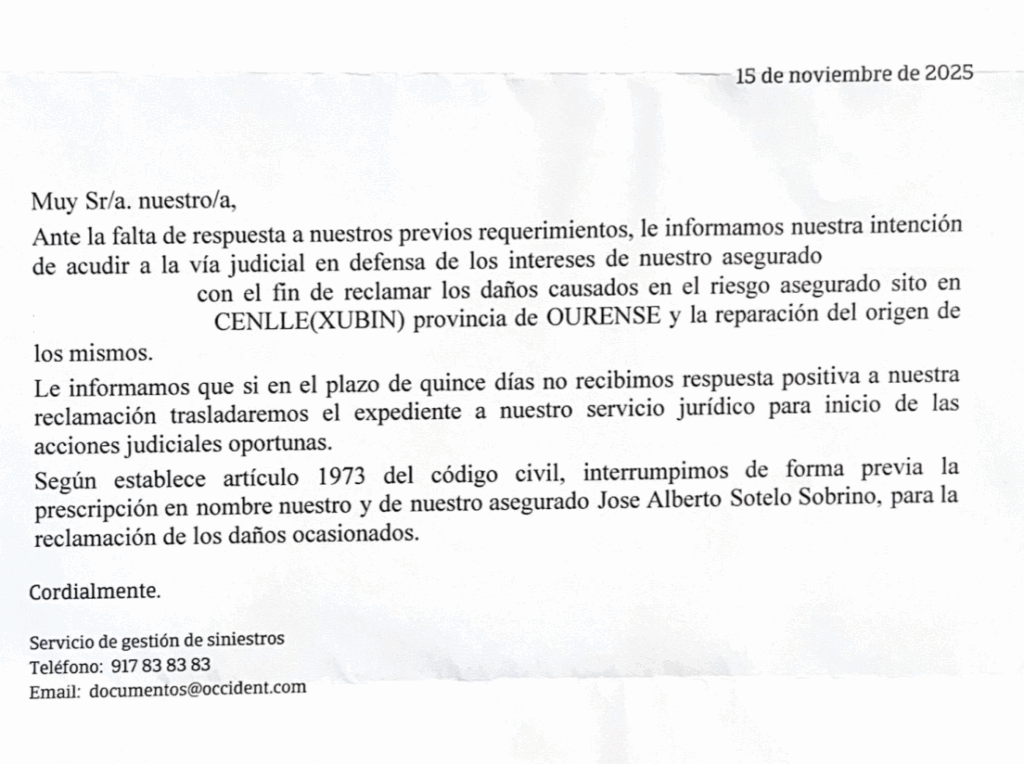

Suddenly, one day our lawyer receives a document called “Claim Report” in which, basically, we are required to pay €711.26 because, according to them, the dampness comes from our plot.

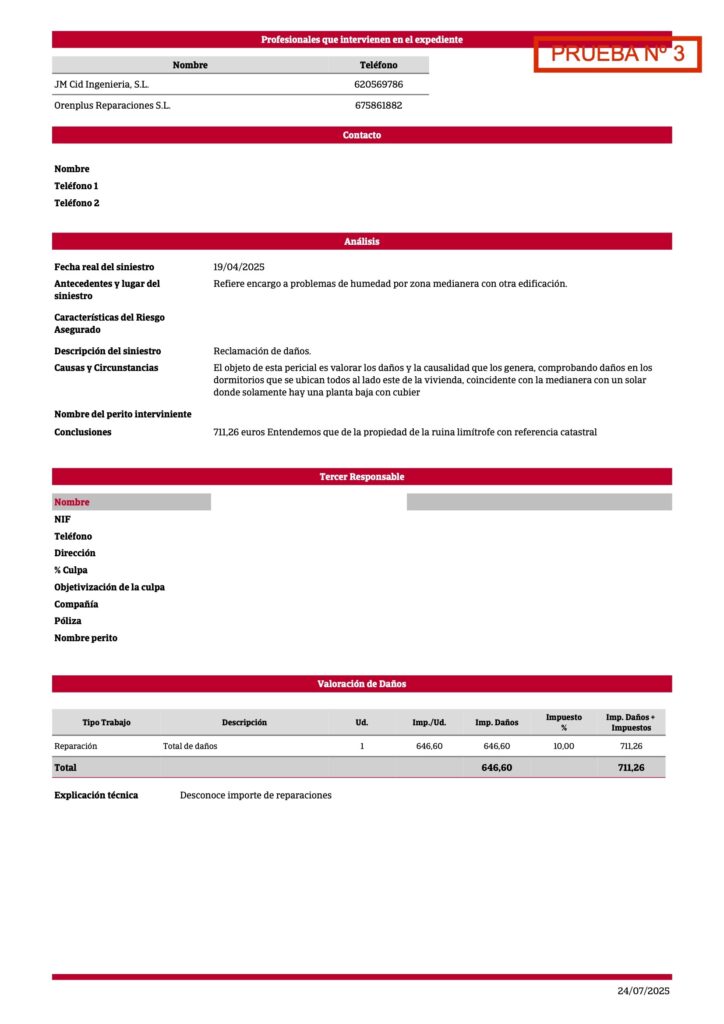

This report is not signed by any expert. There is no name, no professional license number, no analysis, no humidity measurements, no methodology, no serious inspection—nothing.

It is just a piece of paper that repeats what the neighbor says and concludes with “We understand that…,” as if a financial claim could be based on “we understand.”

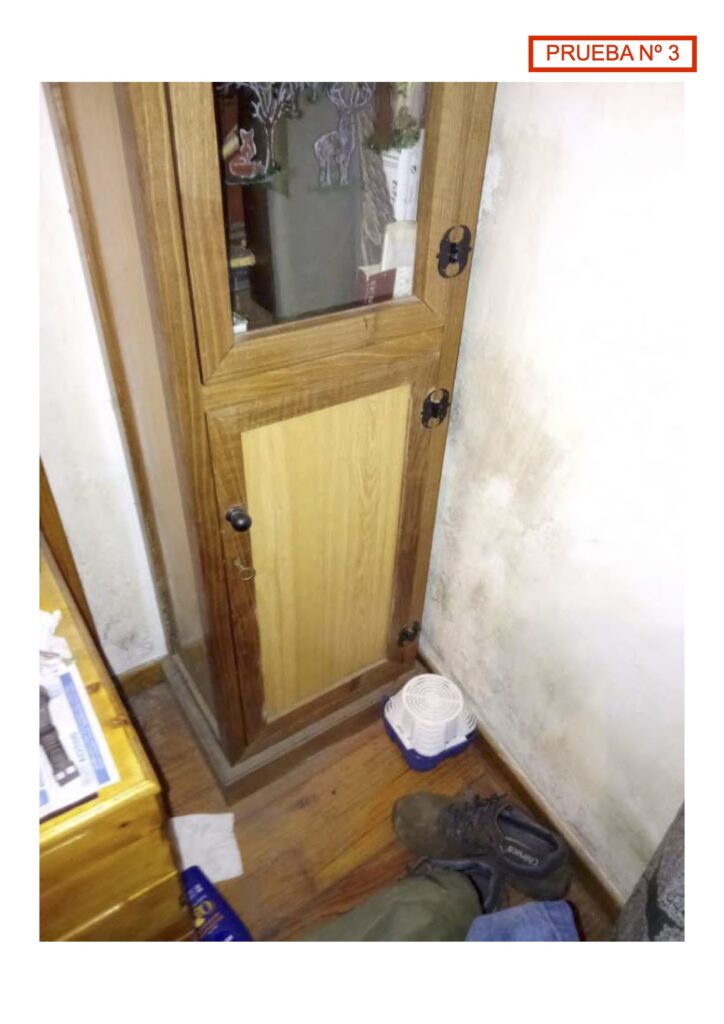

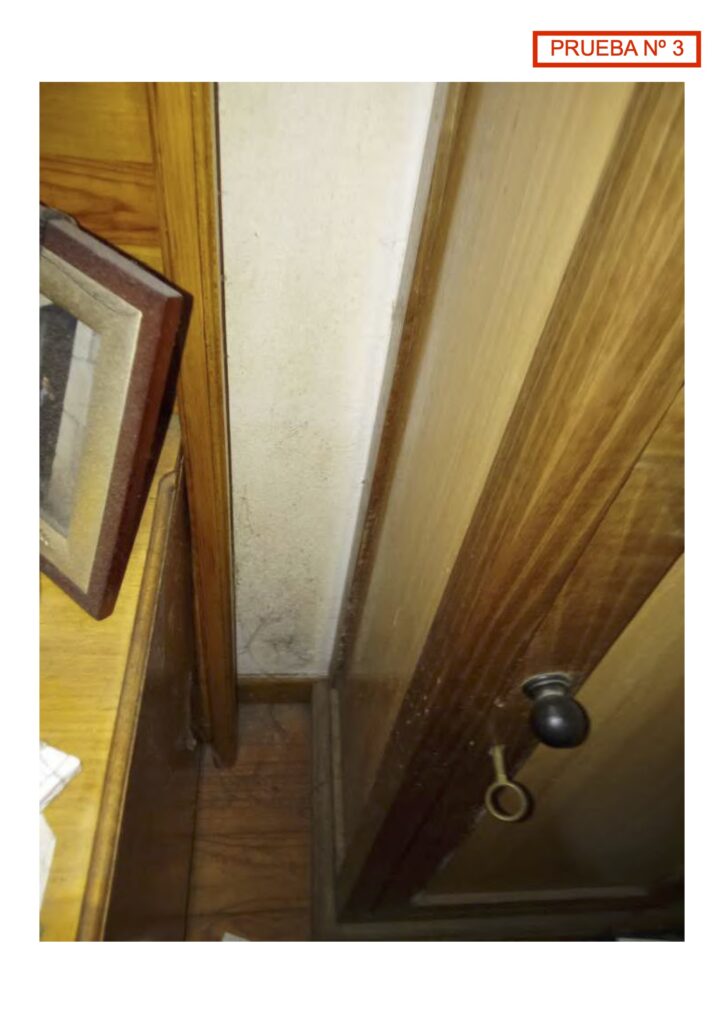

It includes photos taken from inside our property, which means someone climbed onto our wall to take them. We are talking about illegally entering private property.

Even though OCCIDENT knew that we had legal representation they began sending letters directly to our home. Intimidating letters, demanding money, threatening legal action, and telling us that we had to “proceed to repair the origin.”

The origin of what? No technical report, no evidence, nothing. Just the policyholder’s word.

The most surreal part is that we are not even OCCIDENT customers. We have never given them our data. We have never authorized anything. And yet they have used our name, our ID number, and our address to send us intimidating letters.

Because of all this, on November 2, 2025, we took two steps:

- We filed a complaint with the Directorate-General for Insurance and Pension Funds (DGSFP) for insurance malpractice, harassment, unfounded claims, and disregard for legal representation.

- We filed another complaint with the Spanish Data Protection Agency (AEPD) for the improper use of our personal data and for taking images from inside our property without consent.

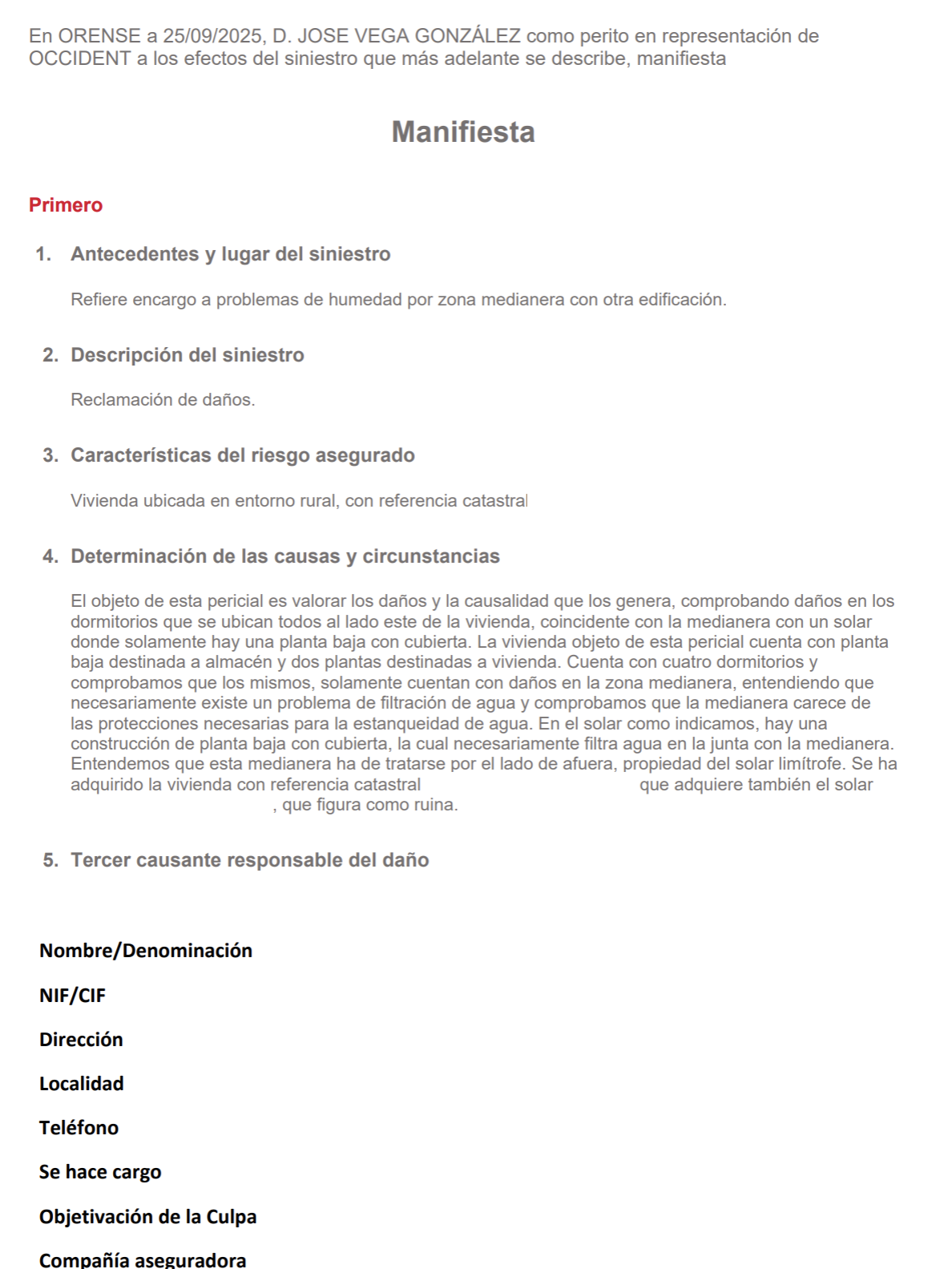

On November 13th, 2025, we received an email from our lawyer: the insurance company OCCIDENT had sent a “new” document which, this time, they presented as an expert/judicial report. What is striking is that this document had never been mentioned during months of claims, burofaxes, and letters. It only appears now, exactly after we filed the formal complaints.

The file arrives in a different format, with a scanned signature and a blurry stamp, attempting to convey a seriousness that it completely lacks. Upon analysing it in detail, we discovered that it is nothing more than a re-formatted version of the old “claim report”: same narrative, same assumptions, the same amount of €711.26, and the same “we understand that…” which the insurer has been repeating for months without providing a single piece of technical evidence.

What is concerning is that this supposed expert report still does not include anything that would make it a real technical report. There are no measurements, no valid inspection, no methodology, no moisture analysis. There is no electronic signature proving the date or authorship. There is no clear professional identification or collegiate endorsement. Nor is there any record of an inspection of our property, which is essential when attempting to attribute the moisture damage in one home to the neighboring one. And above all, they do not rule out any of the possible internal causes that the insured party’s own home might have like capillarity, condensation, structural problems, waterproofing failures, etc.

Everything continues to rely exclusively on the policyholder’s account, without a single objective fact to support the conclusions. And conveniently, this document —supposedly dated September 25th— only appears now. As it does not contain a digital signature, there is no way to verify that it was truly issued on the date they claim.

Given this situation, we have submitted a new extension of our complaint to the DGSFP, explaining why this document cannot be considered a valid technical report.

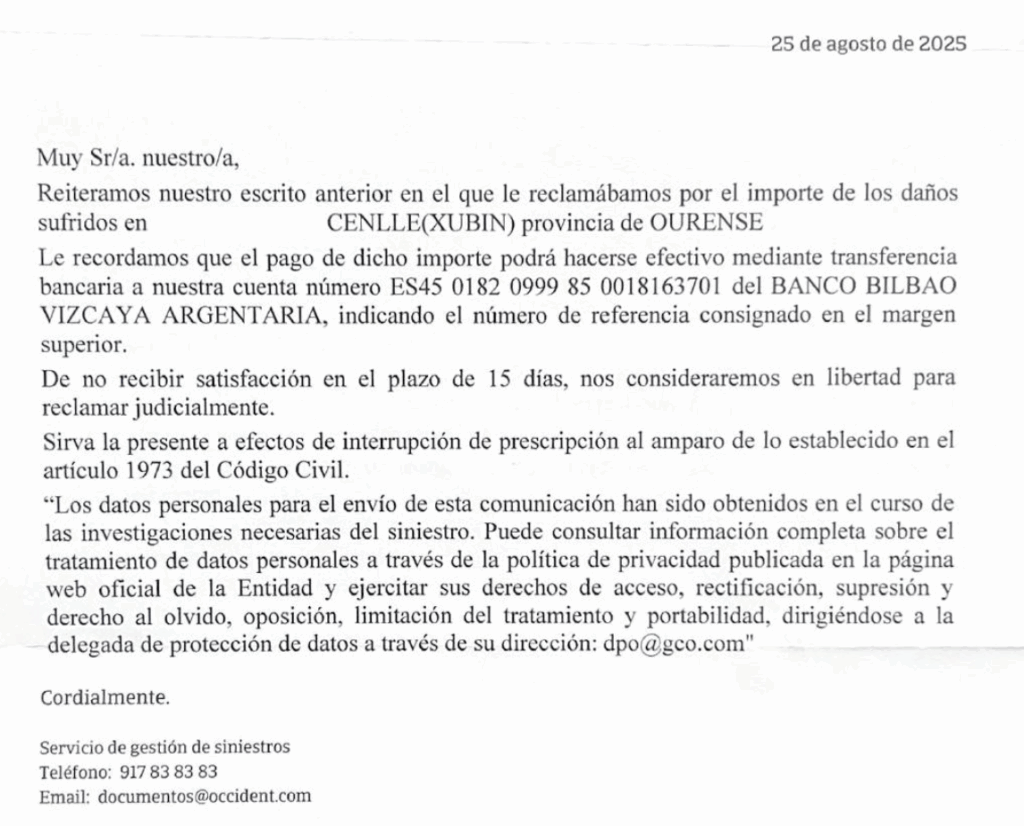

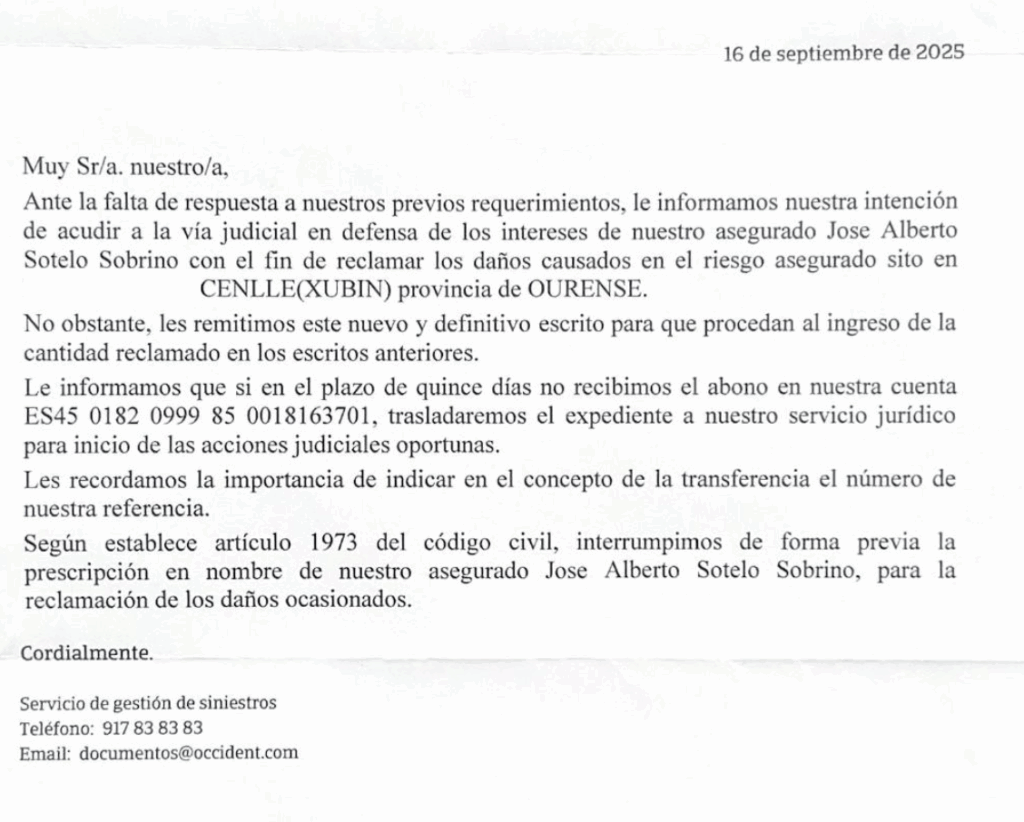

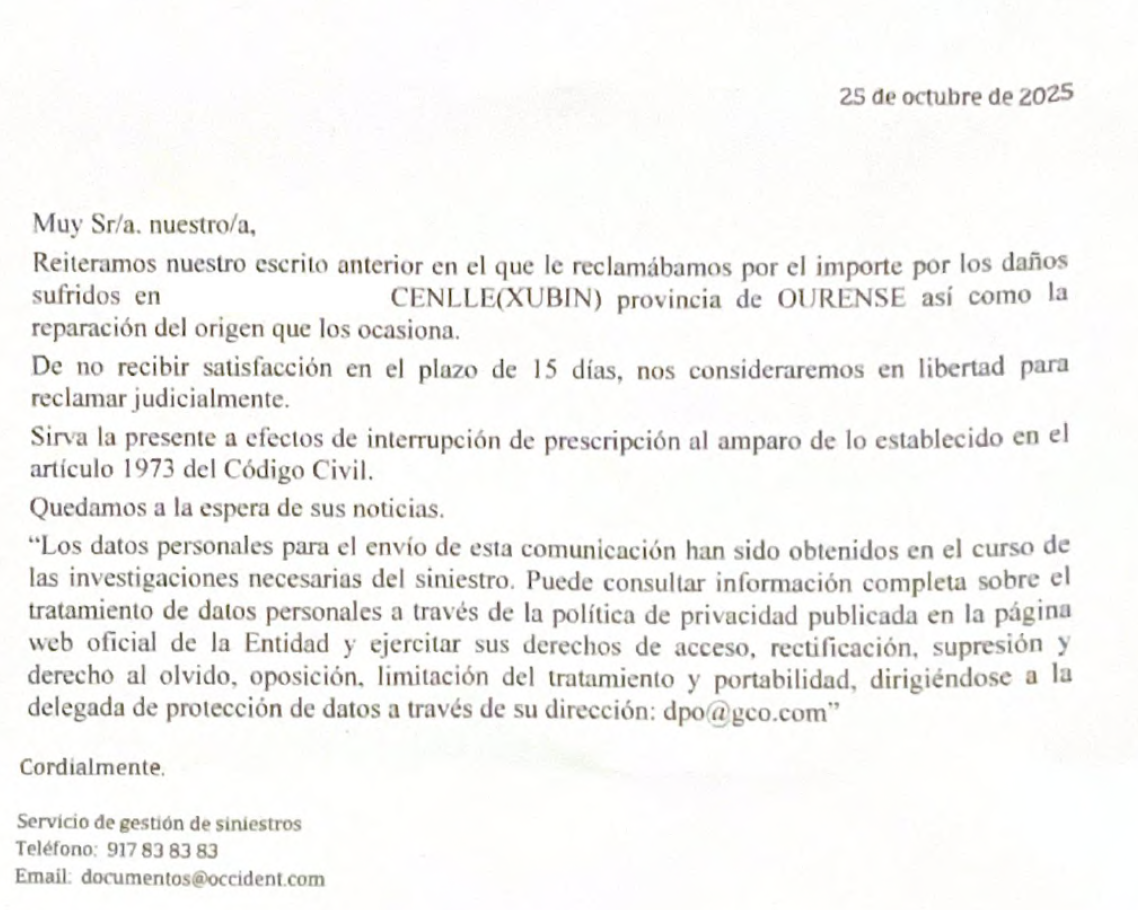

The last weekend of November we went to the house in Ourense, and, on November 29, we found yet another letter. It was practically the same text as always, pressuring us once again to pay the amount they are claiming and warning —again— that if we didn’t do so, in 15 days they would begin legal action.

As you have already been able to read throughout this post, they have been repeating the same threat since August, saying they would sue“in 15 days” if they didn’t receive the payment.

We received the response from the DGSFP, where they told us that, before filing a formal claim with them, we had to first exhaust the internal process: that is, file a complaint with the Customer Service department and wait a period of one month for a response. If the reply was unfavourable, or if they simply did not respond within that period, then we would be able to file the complaint with the DGSFP.

For that reason, on December 1 we proceeded to file the complaint with the Customer Service department, from that point on, we waited to see what would happen once the month had passed.

During the weekend of December 12, we did not find any actual letter from Occident, but we did find a notice of an attempted delivery of a shipment coming from Madrid and sent by the insurance company. It could have been a response to the complaint we had submitted, or a new communication with an intimidating tone, like the previous ones. In any case, it seemed rather illogical to us that they continued to address us directly when they already knew that we had legal representation.

We went to the Civil Guard to ask about the possibility of filing a complaint against the insurance company. They explained to us that they could accept the complaint, but that it would not go anywhere, since for the moment it was a matter of a civil nature, not a criminal one. According to what they told us, the actions of the insurance company could not yet be considered harassment.

To claim any type of liability, the appropriate route was the civil court. In Spain, if an amount greater than 2,000 euros is claimed, it is mandatory to do so with a lawyer. At that point, in mid-December, we still did not know whether there was sufficient legal basis to file a complaint against the insurance company or whether we were entitled to request any compensation.

Before taking that step, we needed something fundamental: the responses from the competent bodies. On the one hand, the Spanish Data Protection Agency, and on the other, the Directorate-General for Insurance and Pension Funds (DGSFP). The procedure first requires waiting for the response from Occident’s customer service department. Only if they did not resolve the situation could we then escalate the complaint to the DGSFP.

Once the complaint had been submitted, it would be necessary to wait and see whether this body considered that there had been an infringement and whether it would impose any penalty on the insurance company. Only if both the Spanish Data Protection Agency and the DGSFP ruled in our favor would it make sense to file a civil lawsuit seeking compensation.

At the end of December 2025, we stopped receiving any further threatening letters or payment demands. No new communication was sent to our lawyer either. Faced with this sudden silence, we understood that perhaps the complaint had served for the central office of the insurance company to detect the irregularity that was taking place in the handling of this alleged insurance claim.

My personal impression is that Margarita may have relied on the collaboration of someone she knew within the local office of the insurance company to try to push forward a claim that, from the very beginning, lacked any legal basis.

Thus, at least for now, the problem has been left on hold, and awaiting definitive closure.

In February 2026, we received the response from the Spanish Data Protection Agency. The authority concluded that, in accordance with current legislation, the insurance company had not breached data protection regulations.

The insurance company may process and use the personal data of someone who is not its client when it intends to file an insurance claim, even if that person has no contractual relationship with the entity. In other words, they can use your data to pursue a claim against you on behalf of their insured party, even when liability has not been proven.

After receiving no response from Occident’s customer service, we once again filed a complaint with the Directorate-General for Insurance and Pension Funds. We were informed that we had to resend the complaint to a different email address.

On 13 February 2026, we sent all the documentation once again to the new email address provided.

More articles on searching for and buying our second home: